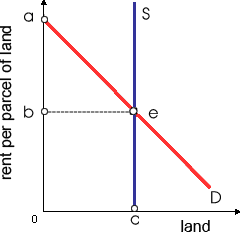

When the resource market shown in this illustrated figure is initially within equilibrium along with demand curve D0: (w) owners of these resources currently receive no economic rents. (x) economic rent is specified by area Oaec. (y) the area bae measures producer surplus by the final output. (z) economic rent equals area Obec.

How can I solve my Economics problem? Please suggest me the correct answer.