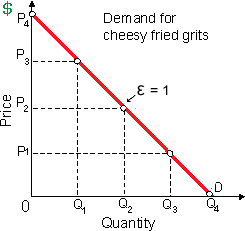

A price increase for Pixie’s cheesy fried grits by P1 to P2 would yield higher total as: (w) revenue because demand is price elastic. (x) supply since demand is unitarily elastic. (y) revenue since demand is price inelastic. (z) use of the good relative to its substitutes.

Can anybody suggest me the proper explanation for given problem regarding Economics generally?