Least probable resource for supply curve

The resource least probable to conform to the supply curve demonstrated in this figure would be: (w) land. (x) capital. (y) labor. (z) entrepreneurship. Can anybody suggest me the proper explanation for given problem regarding Economics generally?

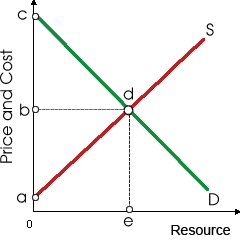

The resource least probable to conform to the supply curve demonstrated in this figure would be: (w) land. (x) capital. (y) labor. (z) entrepreneurship.

Can anybody suggest me the proper explanation for given problem regarding Economics generally?

is the price in the "law of demand" a relative price or an absolute price

Can someone please help me in finding out the accurate answer from the following question. The price per mile of mass transit has increases much rapid since the year 1980 than the price of private auto travel. This has contributed to the shift in demand

Into this "kinked-demand" model, such firm views the marginal revenue curve this faces as the: (1) linear curve acD2 for all prices. (2) linear curve deMR1 for all prices. (3) nonlinear curve adeMR1. (

Jared does not care regarding his job as he is eligible for the unemployment compensation; therefore he frequently goofs off at work and exhibits up late. This is the trouble of: (i) Adverse selection. (ii) Efficiency salaries. (iii) Moral hazard. (iv) Symmetric infor

The law of supply is graphically exhibited by the supply curve which is: (1) Moving all along the demand curve. (2) Vertical. (3) Upward-sloping. (4) Downward-sloping. Can someone please help me in finding out the

For the firm, the major goal of profit sharing plans is to: force workers to incur some of the business risk. overcome the monopsony problem of having to pay higher wages to attract additional workers. overcome the principal-agent problem by better aligning the workers' interests with

Can someone please help me in finding out the accurate answer from the following question. The value of marginal product of the variable resource is its marginal product multiplied by: (1) The marginal revenue from sale of its addition to the output. (2) The price of

A purely competitive firm: (w) faces a perfectly inelastic demand curve. (x) sets its own price. (y) is a price taker. (z) sells a differentiated product. Can someone explain/help me with best solution about proble

Demand is perfectly price elastic when the price for Pixie's cheesy fried grits is a mostly unmeasurably small bit below the: (1) zero. (2) P1. (3) P2. (4) P3. (5) P4. Q : Economic losses generate competitive Economic losses in an industry generate competitive pressures which cause: (1) industry output to fall. (2) market price to decrease. (3) each firm’s short-run output to increase. (4) rising costs for industry inputs. (5) firms to expand product

Economic losses in an industry generate competitive pressures which cause: (1) industry output to fall. (2) market price to decrease. (3) each firm’s short-run output to increase. (4) rising costs for industry inputs. (5) firms to expand product

18,76,764

1956299 Asked

3,689

Active Tutors

1433783

Questions Answered

Start Excelling in your courses, Ask an Expert and get answers for your homework and assignments!!