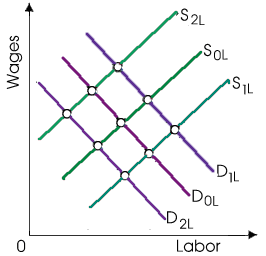

When this purely competitive labor market is primarily in equilibrium at of D0L, S0L, a shift to equilibrium at D2L, S0L would be probably to follow by increases in: (1) minimum wage laws. (2) imports of this good from foreign competitors. (3) workers' desires for leisure as well as willingness to sacrifice extra income. (4) general training of these workers. (5) the depreciation rate for capital used through these firms because of obsolescence.

Can someone explain/help me with best solution about problem of Economics...