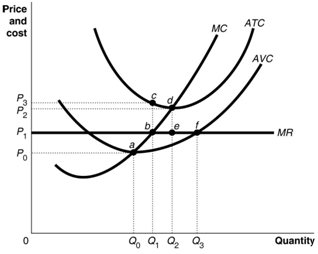

A firm's total profit can be computed as all of the given except w) total revenue minus total cost. x) average profit per unit times quantity sold. y) (price minus average total cost) multiply with times quantity sold. z) marginal profit times quantity sold.

How can I solve my economics problem? Please suggest me the correct answer.