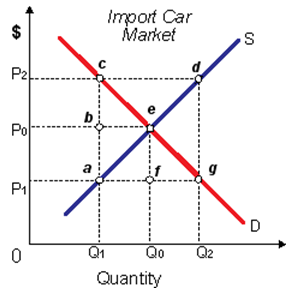

Buyers' demand prices would be ____ and sellers' supply prices would be ____ when the U.S. restricted car imports to Q1. (w) P2 and P1. (x) P0 and P2. (y) P0 and P2. (z) P1 and P2.

Can anybody suggest me the proper explanation for given problem regarding Economics generally?