Black Manufacturing Company

Black Manufacturing produced a single product called the Great Beast. During the past three weeks, Lee High, the new cost accountant, had observed that production efficiency and input prices were constant but that output varied considerably. These three weeks were thought of as typical by sales representative, who said that they could be taken as average. Production costs were accumulated and accounted for under several different groups listed below.

Lee High thought that this would be an ideal time to do some cost analysis on the Great Beast. Based on the data for three weeks' production costs, he felt it would be possible to identify fixed costs, variable costs, and semi-variable costs. Furthermore, Lee wanted to develop some equations that might be useful for managerial decision making. From such equations, it seemed that break-even volume could be generated. Since production was usually based on orders actually received and since products were shipped immediately upon completion, inventories of work-in-process and finished goods were practically nonexistent. When talking to the sales representative, Lee discovered that on typical orders the selling price of Great Beast was $7.00. During lunch one day, Lee was told by the president that office expenses, including certain selling items, were fixed at $781 per week.

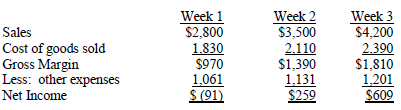

Lee High decided to begin his analysis with income statements from the past three weeks:

From these statements, Lee realized that selling more added to profit. He also realized that cost of goods sold per unit seemed to fall as output rose:

- When sales were 400, then cost of goods sold per unit was $4.58.

- When sales were 500, then cost of goods sold per unit was $4.22.

- When sales were 600, then cost of goods sold per unit was $3.98.

Lee wasn't sure why cost of goods sold per unit should fall, because, after all, the efficiency and input prices had remained the same. He reasoned that there was something odd about the data and decided it would be good to work with some average. Since the three weeks for which Lee had data were thought to be typical, he decided that some "standardized cost information" based on sales of 500 units per week would be very helpful. He derived the following chart:

Useful Data on Great Beast

Average variable cost per unit produced $ 2.80

Average fixed cost per unit produced 1.42

$ 4.22

Average fixed administrative and selling cost per unit 1.56

Commission per sold .70

$ 6.48

Added amount for rounding error and some funny result in data .12

$ 6.60

The following should be kept in mind when selling Great Breast:

1. It costs us $6.60 to deliver a unit of Great Beast, so we make only 40 cents per unit at $7.00 selling price.

2. Decision rule #1 (for sales representative on the road): Never sell Great Beast for less than $6.60 plus a profit margin because at $6.60 we just break even.

3. Decision rule #2 (for direct office sales on which no commission is paid): Never sell Great Beast for less than $5.90 plus a profit margin because at $5.90 we just break even.

Lee was very pleased with his chart, particularly the part about different decision rules. When the chart was finished, Lee passed it on to Mr. Charlton Black, who was the owner, president and chief decision maker at Black Manufacturing. Charlton, who was skeptical of "scientific analysis," studied Lee High's chart and underlying data. That night Charlton said to his lawyer, with whom he was having dinner, "I finally have found the kind of practical fast-track analyst I need. This kid, Lee High, has just developed a set of decision rules that will solve all my pricing and profit problems."

The next day Charlton Black sent a memo to the sales representative and others who were involved in pricing Great Beast. Among other things the memo stated, "Everyone should study Mr. High's chart, especially the decision rules he was generated through complex cost accounting procedures. From now on, all pricing decisions will follow these rules, and under no condition will we price at less than 10% above our delivery cost. Therefore, the lowest prices that can be quoted by the sales representative and office force are $7.26/unit and $6.49/unit, respectively. This new policy means the sales representative had better stop taking orders at $7.00 per unit."

When he read the memo, Lee was both pleased and a bit disturbed. In the first place, he didn't expect Mr. Black to take his chart so seriously; in the second place, he knew intuitively that any price higher than $7.00 per unit for Great Beast was too high. Lee explained his position to Mr. Black, who in turn informed the sales representative that orders at $7.00 would be OK but nothing less would be accepted.

After revision in policy, Lee felt better. Black went on vacation; the sales representative was confused; and the members of the office force, who could take orders by phone, were pleased with their new role.

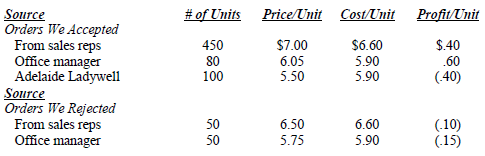

During the next week, the following four sales prospects were available to Black Manufacturing for Great Beast.

1. The sales representative sold 450 units at $7.00 per unit.

2. The sales representative turned down a request from an irregular customer for 50 units at $6.50 per unit because of the $7.00 rule.

3. One telephone order was accepted for $6.50 per unit for 80 units, but another was rejected at $5.75 per unit for 50 units because of the $6.49 rule.

4. Ms. Adelaide Ladywell, a nineteen-year-old file clerk, received a phone call from Maze Woolwich when no one else was in office. Maze said that he had seen Lee high's data on costs, and since Black could produce more economically than Woolwich, he wanted to order 100 units at $5.50. Furthermore, Maze explained that since he was going out of business, this would be his only order. Adelaide said that $6.50 was the minimum price, but Maze responded that that was just Black double-talk. Ms. Ladywell looked over the data and realized that on a special order like this $5.50 would be a good price, considering that otherwise Maze Woolwich would produce the 100 units himself. She accepted the order and anticipated a promotion when Mr. Black returned.

At the end of the week, Lee High prepared the following sales-cost report for Mr. Black.

After Mr. Black looked over the report, he did two things:

1. He called in the sales representative and explained that it would be better for the company to sell 350 units at $8.00/unit than the 450 at $7.00/unit. He went on to say that at $8.00/unit, he would pay a commission of 15% instead of 10%. His reasoning was as follows:

$ 8.00 Revenue $ 7.00 Revenue

Cost per unit per lee chart Cost per unit per lee chart

5.90 5.90

$ 2.10 Contribution $ 1.10 Contribution

1.20Commission .70 Commission

$.90 Clear profit per unit $ .40 Clear profit per unit

350 unit times 90 cents per unit = 450 units times40 cents per unit =

$315 profit per week $1 80 profit per week

The sales representative was instructed to sell at $8.00 and guaranteed at least a commission of 15% on the sales of 350 units.

2. Black fired Adelaide Lady well over the Maze Woolwich mess. He said, "No one is going to cause me to lose 40 cents per unit."

REQUIREMENT: What do you think about the whole situation? Develop a proper quantitative analysis.