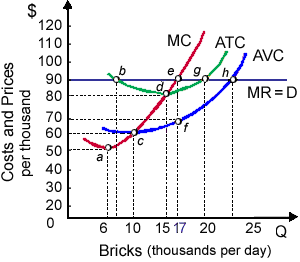

When brick-making is a constant cost industry, during the long run this firm is probable to experience: (i) a severe shrinking of economic profit to zero. (ii) a decline in the price of bricks to approximately eight cents apiece. (iii) increased competition as new firms enter the brick-making industry. (iv) a reduction in the brickyard’s equilibrium output. (v) All of the above.

I need a good answer on the topic of Economics problems. Please give me your suggestion for the same by using above options.