Changes in total revenue by price falls

When the price falls along such demand curve for pizza, in that case total revenue: (w) falls. (x) rises, then falls. (y) rises. (z) does not change. Can anybody suggest me the proper explanation for given problem regarding Economics generally?

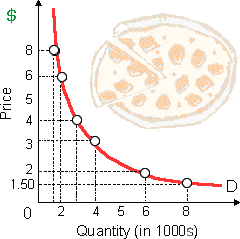

When the price falls along such demand curve for pizza, in that case total revenue: (w) falls. (x) rises, then falls. (y) rises. (z) does not change.

Can anybody suggest me the proper explanation for given problem regarding Economics generally?

The only supply curve which has price elasticity which varies as the price of output increases is within: (w) Panel A. (x) Panel B. (y) Panel C. (z) Panel D. Q : Greater economics loss than fixed costs Within the short run, there a monopolistically competitive firm will NOT operate at: (w) an economic loss that is less than fixed costs. (x) an economic loss that is greater than fixed costs. (y) making a normal profit. (z) making economic profits.

Within the short run, there a monopolistically competitive firm will NOT operate at: (w) an economic loss that is less than fixed costs. (x) an economic loss that is greater than fixed costs. (y) making a normal profit. (z) making economic profits.

I have a problem in economics on Imperfect competition problem. Please help me in the following question. As MRP < VMP in the imperfect competition whenever firms have market power as the sellers: (1) MPPL = VMP. (2) Price of output surpasses MFC.

Profit is maximized when this purely-competitive brickyard constructs at: (i) point a. (ii) point b. (iii) point c. (iv) point d. (v) point e. Q : Yield behaviour conflicting law of Which of the given statements, if true, seems most probable to yield behavior which would conflict with the law of demand? (i) People cannot afford to drive as much whenever the price of gasoline goes above $3.00 per gallon. (ii) The greater heroin addicts encompass i

Which of the given statements, if true, seems most probable to yield behavior which would conflict with the law of demand? (i) People cannot afford to drive as much whenever the price of gasoline goes above $3.00 per gallon. (ii) The greater heroin addicts encompass i

Short-run profit is maximized only while: (w) economic profit > accounting profit. (x) total cost = total revenue. (y) MC = MR (greater than minimum AVC). (z) costs are minimum or revenue is maximum. How can I s

If comparing monopolistic competition to pure competition within the long run: (w) product differentiation definitely improves social welfare. (x) only monopolistic competitors may earn economic profits. (y) only pure competitors oper

Within the modern U.S. economy, there pure competition is: (w) characteristic of all resource markets. (x) rare in product markets. (y) most common for public utilities. (z) strictly regulated throguh government. I

The percentage change within quantity supplied divided through the percentage change within price is an approx measure of a good's: (w) unitary margin. (x) price elasticity of supply. (y) exclusivity ratio. (z) price elasticity of demand. Q : Key questions in evaluating a research Key questions in evaluating a research report: In brief, there are five key questions you, as a consumer of analytical work, should ask yourself as you are evaluating a research report. 1. What is the purpose of th

Key questions in evaluating a research report: In brief, there are five key questions you, as a consumer of analytical work, should ask yourself as you are evaluating a research report. 1. What is the purpose of th

18,76,764

1923729 Asked

3,689

Active Tutors

1431746

Questions Answered

Start Excelling in your courses, Ask an Expert and get answers for your homework and assignments!!